Running a yoga studio feels like financial whiplash sometimes. January floods you with New Year's resolution members, March brings spring break cancellations, summer sees both teacher vacations and student dropoffs, then September kicks back up with back-to-school energy. Meanwhile, your rent stays exactly the same every single month.

The studios that make it past year three aren't necessarily the ones with the best teachers or the prettiest spaces. They're the ones who stopped treating cash flow like a monthly surprise and started treating it like something they could actually predict and manage.

Most studio owners track revenue and expenses, sure. But tracking what happened last month doesn't help when you need to decide whether you can afford that new reformer in April or if you should wait until after the summer slowdown. What you really need is a rolling view of what's coming, not just what passed.

Why standard business budgets fail yoga studios

Traditional annual budgets assume steady monthly revenue. That works fine for subscription software companies or dental practices with recurring patients. It's useless for studios where December revenue might be 40% lower than January's.

Seasonal swings hit yoga studios harder than most small businesses because you're dealing with multiple overlapping cycles - the obvious ones like holidays and summer vacations, then local patterns like tourist seasons, university schedules, or harsh winters if you're in that kind of market.

On top of that, your expense timing rarely aligns with revenue. Property taxes hit in April and November. Insurance renewals come once a year. Marketing spend needs to ramp up before slow seasons, not during them. Teacher certifications expire on their own schedules. Equipment breaks when it wants to, not when it's convenient.

A static annual budget can't handle this. By the time you realize March revenue came in 20% below projection, you've already committed to April expenses based on outdated assumptions. Your cash flow calendar needs to be a living document, not a spreadsheet you update once in January and ignore for eleven months.

Building your three-scenario framework

Instead of one "expected" budget, build three scenarios and update them monthly. This isn't about being pessimistic or optimistic - it's about understanding your operational boundaries before you need to.

Eliminate class scheduling chaos.

Yoglyly helps you book, confirm & manage every class seamlessly.

- Centralized class scheduling

- Member notifications

- Instructor and resource management

No credit card required

Your low scenario is survival mode. Typically 70-75% of your trailing twelve-month average. At this level you're covering rent, essential staff, insurance, and utilities. No new equipment, minimal marketing, possibly reduced class schedules. Think summer slump or unexpected closure.

-

Rent

$5,500

-

Core teachers (W2)

$6,000

-

Contractor teachers

$2,000

-

Insurance/licenses

$650

-

Utilities

$450

-

Software/systems

$350

-

Loan payments

$1,200

-

Basic supplies

$200

-

Owner draw

$1,650

The medium scenario sits around 95-105% of your average. Current operations maintained, standard marketing spend, some buffer for maintenance. Most months should land here.

-

Rent

$5,500

-

Core teachers (W2)

$7,500

-

Contractor teachers

$4,000

-

Insurance/licenses

$650

-

Utilities

$450

-

Software/systems

$350

-

Marketing

$1,000

-

Loan payments

$1,200

-

Supplies/maintenance

$500

-

Equipment fund

$500

-

Owner draw

$4,350

Your high scenario - usually 125-130% of average - represents peak months like January or September. This is when you can accelerate equipment purchases, invest in teacher training, or build reserves.

-

Rent

$5,500

-

Core teachers (W2)

$8,500

-

Contractor teachers

$5,500

-

Insurance/licenses

$650

-

Utilities

$450

-

Software/systems

$350

-

Marketing

$2,000

-

Loan payments

$1,200

-

Supplies/maintenance

$500

-

Equipment purchases

$1,500

-

Reserve fund

$2,000

-

Training/development

$500

-

Owner draw

$5,350

Notice how certain expenses stay fixed (rent, insurance, utilities), while others scale with revenue (teacher pay, marketing, owner draw). That's not a coincidence - it reflects actual operational reality. You can't negotiate your rent down when August is slow, but you can adjust class schedules and pull back on ads.

Month-by-month expense mapping

Every studio has predictable expense spikes throughout the year. Missing these in your planning is what causes those "surprise" cash crunches that force you to skip marketing right when you need it most, or delay equipment repairs until they become emergencies.

-

January - Regular monthly expenses - Annual insurance renewal (add $2,400-3,600) - New Year marketing push (add $500-1,000) - Post-holiday payroll catch-up

-

February - Regular monthly expenses - Valentine's/wellness promotions (add $300) - Potential heating costs spike (add $100-200)

-

March - Regular monthly expenses - Spring schedule changes - Teacher training renewals (varies)

-

April - Regular monthly expenses - First quarter tax payments (set aside 25-30% of Q1 profit) - Property tax (if semi-annual) - Spring cleaning/maintenance (add $500-800)

-

May - Regular monthly expenses - Memorial Day reduced schedule - Summer marketing prep (add $500)

-

June - Regular monthly expenses - Mid-year insurance audit - Equipment maintenance before summer

-

July - Regular monthly expenses - Lowest revenue month typically - Second quarter tax payments

-

August - Regular monthly expenses - Back-to-school marketing ramp (add $800-1,200) - Fall schedule preparation - Teacher hiring/training for fall

-

September - Regular monthly expenses - Highest revenue month typically - New student onboarding costs

-

October - Regular monthly expenses - Third quarter tax payments - Holiday schedule planning

-

November - Regular monthly expenses - Property tax (if semi-annual) - Black Friday/holiday promotions (add $500) - Reduced Thanksgiving week

-

December - Regular monthly expenses - Holiday bonuses (varies) - Reduced holiday schedule - Year-end tax planning - Annual renewal prep

These aren't arbitrary. Property taxes land on the same date every year. Insurance renewals are scheduled. Even "surprise" equipment failures usually give warning signs if you're doing routine maintenance and paying attention.

Reserve triggers and decision rules

Reserves aren't just a cushion - they're a decision-making tool. But a pile of money in a savings account without clear rules about when to use it just creates anxiety. Should you dip in for that workshop opportunity? What about when summer revenue drops 30%?

Set specific triggers tied to your operational KPIs:

-

Green zone (3+ months expenses in reserve) - Approve equipment upgrades - Invest in teacher training - Test new marketing channels - Consider expansion opportunities

-

Yellow zone (1.5-3 months in reserve) - Maintain current operations - Postpone non-essential purchases - Focus on retention over acquisition - No new financial commitments

-

Red zone (less than 1.5 months) - Reduce class schedule - Pause all discretionary spending - Negotiate payment plans with vendors - Focus solely on revenue generation - Consider short-term financing options

Your reserve target should be 3-6 months of your low-scenario expenses, not your current average. If your low scenario is $18,000/month, you're aiming for $54,000-108,000 in reserves. That sounds like a lot. It is. But it's what keeps you operational when a key teacher quits suddenly or your HVAC dies in July.

Build reserves through automatic transfers, not willpower.

Every time revenue exceeds your medium scenario, move the excess before you can spend it. Don't wait until the end of the month to "see what's left" - there won't be anything.

Payroll patterns and teacher cost management

Teacher payroll rarely aligns neatly with revenue. Your compensation structure might include hourly W2 employees, per-class contractors, revenue shares, or some mix of all three. Each creates different cash flow patterns.

Hourly W2 teachers give you scheduling stability but create fixed costs whether classes are full or empty. During slow months, you're still paying. This works well for core classes and peak time slots where consistency matters.

Per-class contractors scale naturally with your schedule - fewer classes, lower payroll. But they require higher per-class rates since they're not getting benefits or guaranteed hours. And popular contractors might not be available when you need them during busy seasons.

Revenue-share models align teacher pay with studio performance but add complexity. A teacher at 30% of class revenue might earn $150 from a packed Monday evening and $45 from a slow Tuesday afternoon. Over time that leads to competition for prime slots and avoidance of less profitable but necessary classes.

Most studios that manage this well end up with something like:

-

2-3 core W2 teachers covering 40-50% of classes

-

Contractors for specialty classes and overflow

-

Revenue share for workshops and special events

Track teacher costs as a percentage of revenue, not just total dollars. Above 45% in any given month and you need to adjust scheduling, compensation structure, or pricing. Below 35% and you're probably understaffing, which leads to burnout faster than most owners expect.

Marketing spend timing and seasonal adjustments

Marketing spend needs to happen before you need the revenue. This seems obvious but it's exactly where cash flow pressure causes bad decisions.

August marketing drives September enrollment. December marketing brings January's New Year crowd. If you wait until September to market because "that's when people are ready," you've already missed the window.

-

November/December

Heavy push for New Year (biggest single opportunity most studios have)

-

March

Summer schedule and outdoor classes

-

July/August

Back-to-school momentum

-

Ongoing

Retention and referral programs

Budget 5-8% of projected revenue for marketing during growth phases, 3-5% during stable periods. Spending $2,000 in December to capture January's boom might generate $8,000 in additional revenue. That same $2,000 in February might only generate $2,500. Same budget, very different outcome.

Track cost per acquisition by channel and season. Facebook ads might cost $40 per new student in January but $85 in July. Email campaigns to lapsed members might convert at 12% in September but only 4% in May. This data shapes next year's calendar, which is the whole point.

Tax obligations throughout the year

Quarterly estimated taxes catch more studio owners off guard than anything else. A strong January, reinvestment into the space, then April 15th arrives with a bill you can't cover.

Set aside tax reserves from every deposit, not quarterly:

-

15.3% for self-employment tax (if LLC/sole prop)

-

10-25% for federal income tax (depends on total income)

-

0-10% for state income tax

That's 25-40% of profit going straight to a tax reserve account. Not revenue - profit. If you brought in $30,000 and had $24,000 in expenses, set aside 30% of the $6,000 profit.

Quarterly deadlines don't move:

-

April 15

Q1 (January-March)

-

June 15

Q2 (April-May)

-

September 15

Q3 (June-August)

-

January 15

Q4 (September-December)

Missing these triggers penalties. Underpaying triggers penalties. The fix is consistent monthly set-asides, not scrambling every three months.

Your ready-to-use tracking template

Here's a framework you can copy into your own spreadsheet:

| Month | Low Scenario Revenue | Medium Scenario Revenue | High Scenario Revenue | Actual Revenue (filled as month completes) | Fixed Expenses | Variable Expenses | Special Expenses (from annual calendar) | Total Expenses | Net Cash Flow | Running Reserve Balance | Action Triggers |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Month | Low Scenario Revenue | Medium Scenario Revenue | High Scenario Revenue | Actual Revenue (filled as month completes) | Fixed Expenses | Variable Expenses | Special Expenses (from annual calendar) | Total Expenses | Net Cash Flow | Running Reserve Balance | Action Triggers |

Weekly Checkpoint Questions:

-

Are we tracking toward low, medium, or high scenario?

-

What expenses can we defer if tracking low?

-

What investments should we accelerate if tracking high?

-

Are reserves above or below target?

-

Any upcoming special expenses in the next 30 days?

Daily Cash Position:

-

Starting bank balance

-

Expected deposits today

-

Required payments today

-

Ending position

-

Days of expenses covered

This isn't about perfect prediction. It's about having a framework for decisions. When a teacher asks for a raise, you can check whether you're in green, yellow, or red zone. When equipment needs replacing, you know if it's a "now" or "wait two months" situation.

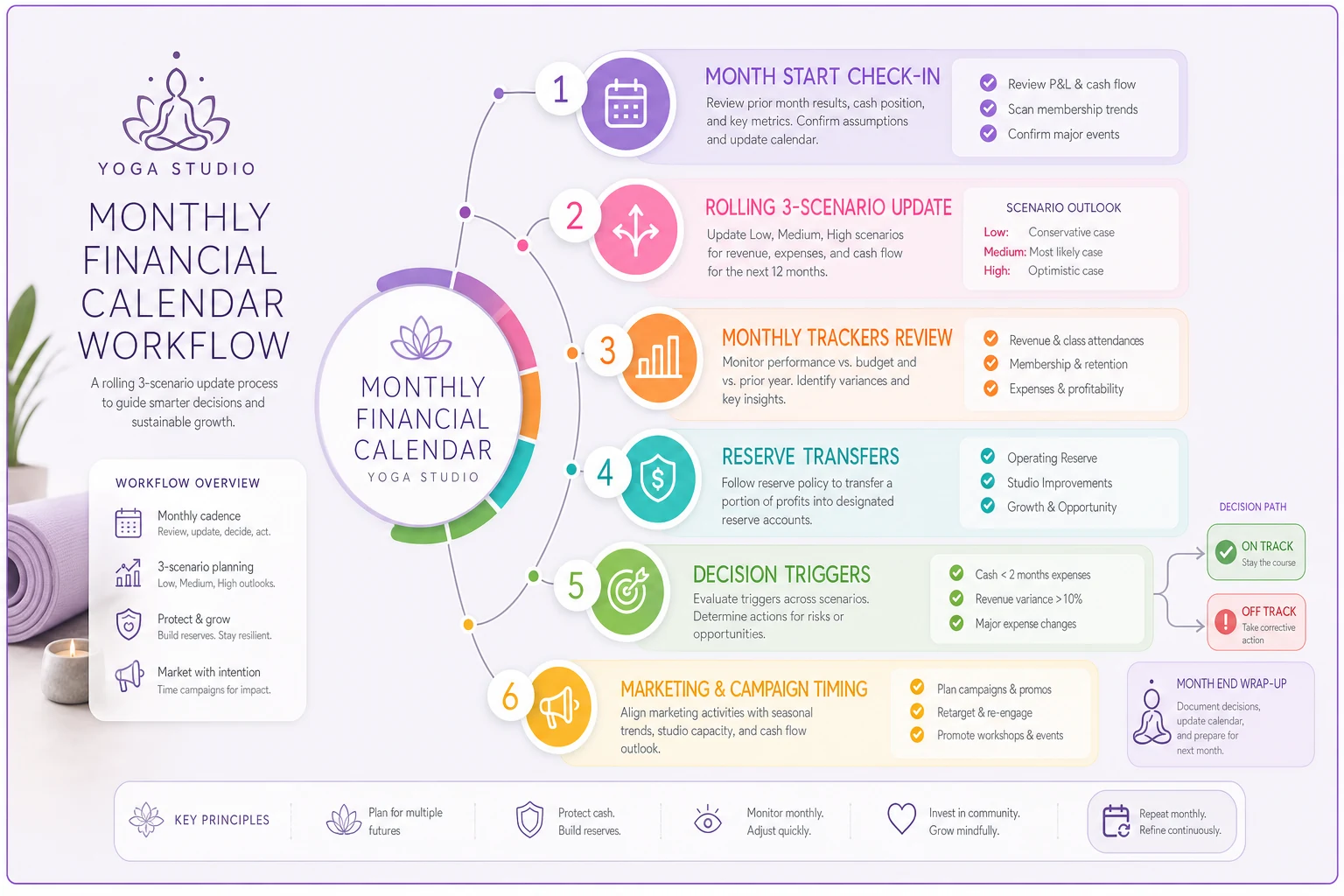

Here's a quick visual to keep the process simple and repeatable.

Use this flow to update scenarios monthly, move excess revenue to reserves, and schedule marketing ahead of peak months.

Technology integration and operational efficiency

Manual cash flow tracking starts breaking down somewhere around 150 monthly transactions. You spend more time updating spreadsheets than actually analyzing anything useful.

Most studios already run multiple software platforms - scheduling, payment processing, payroll, marketing. The problem is they don't connect, so you're pulling reports from each one separately and trying to manually piece together a complete picture. It's slow and it's where errors creep in.

AI-powered operational software can automatically pull transaction data from your payment processor, match it with scheduling data, calculate teacher pay based on attendance, and project next month's cash flow based on current booking patterns. Instead of Sunday nights in spreadsheets, you get a real-time view of your cash position.

The other thing automation does well is surface patterns you'd otherwise miss. Maybe Tuesday evening classes consistently outperform projections because they attract drop-in students who buy packages. Or your workshop revenue is actually more predictable than monthly memberships once you account for seasonality. Those insights only show up when you're analyzing twelve months of integrated data, not spot-checking individual months.

Common cash flow pitfalls and solutions

The biggest cash flow killer isn't low revenue - it's timing mismatches. Rent is due on the 1st, but most membership revenue comes in between the 5th and 15th. Payroll runs on the 15th and 30th, but contractor payments might be weekly. One delayed merchant services deposit can cascade into multiple late payments before you even realize what's happening.

Build timing buffers into your calendar:

-

Keep one full payroll cycle in reserves

-

Negotiate rent payment for the 5th or 10th if possible

-

Stagger large expenses across the month

-

Set up automatic transfers to smooth cash flow

Another quiet problem is membership decay without replacement. A studio with 200 members losing 5% monthly needs 10 new members just to stay flat. Acquisition costs spike during slow seasons - exactly when you most need new people. This creates a spiral where you can't afford marketing when you most need it.

The counter to this is building marketing reserves during strong months to deploy during weak ones. If September brings in $34,000 against $26,000 in expenses, that $8,000 shouldn't go to upgrades. It should fund July and August marketing.

Equipment financing seems manageable right up until it isn't. A $15,000 reformer at $500/month over 36 months sounds fine. But when summer revenue drops 30%, that payment doesn't care. Buying used equipment outright during strong months is almost always better than financing new equipment that puts pressure on weak ones.

From reactive to predictive management

Studios still operating after five years didn't get lucky with consistent revenue. They built systems that assume inconsistency and plan around it.

Your cash flow calendar isn't a constraint - it's a decision-making tool. When you know February will be tight, you can pre-sell March workshops in January. When you see September's surge coming, you can hire and train teachers in August instead of scrambling to add classes after demand already spikes.

This approach transforms cash flow from a monthly unknown into a manageable operational pattern. You stop making financial decisions based on your current bank balance and start making them based on your projected position over the next quarter.

The difference between studios that survive seasonality and those that don't isn't reserve account size or forecast accuracy. It's whether there's a system for making financial decisions that accounts for the natural rhythms of the business. Build that system, maintain it monthly, and cash flow becomes just another operational process - not a crisis to manage around every few months.

Ready to elevate your studio operations?

Join 1,500+ yoga studios using Yoglyly to save time, reduce scheduling conflicts, and enhance member experiences.